Understanding how competitors move, adapt, and position themselves has become a core part of how organizations plan for growth. Competitive intelligence research brings together competitor activity, market signals, and customer behavior to create a clearer view of what’s changing and why. This clarity helps organizations track shifting market dynamics, test assumptions, and make data-driven decisions.

To find out what 949,079 opinions of insights, strategy, or marketing leaders were about competitive intelligence research, Sedulo partnered with Artios to develop this analysis using AI-driven audience profiling to synthesize insights from online discussions over 12 full months ending March 15, 2026, to a high statistical confidence level. These perspectives show how leaders apply competitive intelligence research, where it delivers the most value, and where its impact can be strengthened.

Index

- 55% of insights, strategy, or marketing leaders say that competitive intelligence research plays a limited role in long-term strategic planning

- Marketing strategy refinement is the primary goal for 37% of leaders using competitive intelligence research

- 48% of insights, strategy, or marketing leaders say that competitive intelligence research is extremely beneficial for their brand positioning strategy

- 43% of insights, strategy, or marketing leaders say they use competitive intelligence research to shape their customer experience strategy

- 100% of insights, strategy, or marketing leaders’ internal research teams currently gather competitive intelligence research insights

- 56% of insights, strategy, or marketing leaders say that AI is not currently used in their competitive research process

- 40% of insights, strategy, or marketing leaders say that their organization continuously reviews competitive intelligence insights using monitoring tools

- 82% of leaders say their organization uses research reports to share competitive intelligence research insights internally

- 80% of leaders say that market expansion and growth strategy is the competitive insight area that gets the most attention in their organization

- 100% of insights, strategy, or marketing leaders monitor strategic partnerships as a top priority

- 54% of leaders say that talent hiring trends are the earliest indicator of competitive change

- 73% of leaders agree that product strategy insight provides the most value for their teams

- For 44% of leaders, The Wall Street Journal provides the most valuable competitive insights for teams

- Fragmented information sources are only somewhat of a challenge that limits the effectiveness of competitive intelligence research for 8% of leaders

- 59% of insights, strategy, or marketing leaders say that deeper competitor analysis would make a huge difference to the value of competitive intelligence research in their organization

- 100% of leaders agree that strategic insight presentations would be a fairly actionable format for making it easier for leadership teams to act on competitive intelligence insights

- 87% of insights, strategy, or marketing leaders operate in the manufacturing and industrial sectors

- 47% of insights, strategy, or marketing leaders’ organizations are primarily based in San Francisco

- Leaders Are Using Insight to Stay Ahead of Market Change

- About The Data

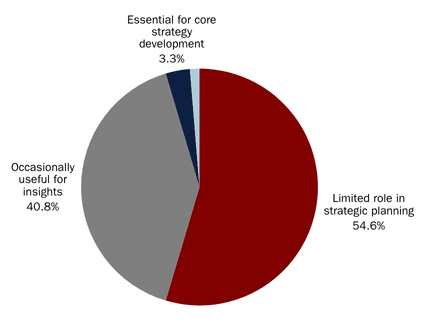

How Important Is Competitive Intelligence Research For Long Term Strategic Planning?

55% of insights, strategy, or marketing leaders say that competitive intelligence research plays a limited role in long-term strategic planning

Opinions on long-term planning differ somewhat:

The importance of competitive intelligence research for long-term strategic planning among leaders is still taking shape. 55% of our audience say it plays a limited role, while 41% find it occasionally useful for insights, signaling that it is more commonly used to support decision-making than to shape long-term direction.

A recent report on competitive intelligence as a lever of added value identifies why this may be the case, highlighting challenges such as embedding CI into organizational culture, building consistent data collection and analysis processes, and developing the analytical skills needed to apply insights effectively.

Only 3% consider it essential for core strategy development, and a further 1% describe it as helpful for planning discussions, suggesting that few teams place it at the center of strategic planning.

Sedulo Commentary: While many organizations still treat competitive intelligence as a supporting input, Sedulo views CI as most powerful when it is embedded directly into long-term strategic planning. When intelligence is connected to business priorities, it can help leaders move from reactive decision-making to more proactive, market-informed strategy.

What Primary Goal Drives Your Use Of Competitive Intelligence Research?

Marketing strategy refinement is the primary goal for 37% of leaders using competitive intelligence research

Some goals are more prevalent than others:

The overarching goal of insights, strategy, or marketing leaders when using competitive intelligence research is to refine marketing strategies. 23% say that is their top priority, while 14% say it’s an important factor, pointing to just how crucial data-driven marketing decisions are.

16% of our audience says that competitive positioning improvement is their top priority, 4% agree it’s a significant factor, and 15% and 3% share the same sentiments about market trend understanding. Just behind at 12% are those who say strategic planning support is their top priority, followed by 2% who feel the same about product development insight, and another 9% who say this is an important factor.

These opinions show that while refining marketing strategy remains the leading priority, competitive intelligence is valued across multiple areas of decision-making, from positioning and trend analysis to long-term planning and product development.

Sedulo Commentary: Sedulo sees this as a reminder that competitive intelligence should not only inform marketing decisions, but also connect positioning, product, customer, and growth strategy into a clearer view of the market. The greatest value comes when CI moves beyond individual use cases and helps teams align around where to compete, how to differentiate, and how to act.

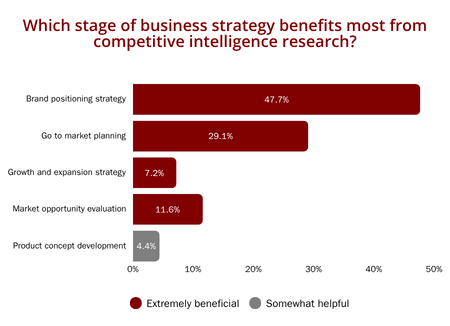

Which Stage Of Business Strategy Benefits Most From Competitive Intelligence Research?

48% of insights, strategy, or marketing leaders say that competitive intelligence research is extremely beneficial for their brand positioning strategy

Business strategy benefits are widespread:

For our audience, brand positioning strategy is the business strategy stage that benefits most from competitive intelligence research. 48% say it’s extremely beneficial, showing how closely CI supports defining competitive context and differentiation. A Harvard Business School guide to brand positioning points out that strong positioning depends on clearly identifying a brand’s competitive set, point of difference, and supporting proof. Competitive intelligence feeds directly into that work by helping teams understand rivals and sharpen how they stand apart.

Go-to-market planning is extremely beneficial for 29%, as CI helps teams anticipate competitor moves, refine messaging, and time launches more effectively. Market opportunity evaluation is extremely beneficial for 12%, as intelligence helps identify gaps and assess demand.

Growth and expansion strategy is extremely beneficial for 7%, with CI helping teams assess new markets and competitive risks. Product concept development is somewhat helpful for 4%, indicating that intelligence plays a lighter role in early-stage idea formation than in later strategic decisions.

Sedulo Commentary: Sedulo agrees that brand positioning is one of the clearest areas where competitive intelligence can create value, because strong positioning depends on understanding both the customer and the competitive set. The strongest CI programs go further by connecting positioning insights to go-to-market planning, growth strategy, and product decisions.

How Is Competitive Intelligence Research Used Within Your Organization?

43% of insights, strategy, or marketing leaders say they use competitive intelligence research to shape their customer experience strategy

The use of competitive intelligence research within organizations varies:

The way competitive intelligence research is used within organizations is led by customer experience strategy. 43% of insights, strategy, or marketing leaders apply it here, showing how closely CI supports understanding customer expectations and competitor benchmarks. A PwC report on the future of CX highlights why this matters: 73% of consumers cite customer experience as a key factor in purchasing decisions, yet only 49% say companies deliver a good experience today. This gap creates a clear need for better insight into customer needs and competitive performance.

Product roadmap development is used by 23%, where CI helps teams prioritize features based on competitor offerings and emerging market expectations. Marketing campaign planning is also used by 23%, with intelligence shaping messaging, positioning, and channel choices to stand out in crowded markets.

Executive strategy planning accounts for 11%, suggesting CI plays a more selective role at the highest level, where it informs direction but is balanced alongside broader commercial considerations.

Sedulo Commentary: Sedulo sees customer experience as a natural application for competitive intelligence, because understanding how competitors engage, serve, and retain customers can reveal meaningful opportunities for differentiation. The most effective organizations use these insights not just to benchmark the customer experience, but to identify where they can deliver greater value than the market currently offers.

How Does Your Organization Currently Gather Competitive Intelligence Research Insights?

100% of insights, strategy, or marketing leaders’ internal research teams currently gather competitive intelligence research insights

When it comes to how organizations are gathering competitive intelligence research insights, it’s clear that leaders are relying on internal research teams. This points to a preference for in-house expertise; however, it may stem from a lack of awareness of other options and of how outsourcing can yield even better, more conclusive, and more comprehensive results.

Sedulo Commentary: Sedulo recognizes the value of internal research teams but believes the strongest competitive intelligence programs often combine internal context with external perspective and specialized primary research. This balance helps organizations validate assumptions, uncover harder-to-find insights, and turn fragmented signals into more actionable strategy.

How Is Artificial Intelligence Used In Your Competitive Intelligence Research Process?

56% of insights, strategy, or marketing leaders say that AI is not currently used in their competitive research process

Use of AI is not yet widespread:

The way our audience uses artificial intelligence in the competitive intelligence research process is still developing. While Stanford University’s 2025 AI Index Report found that AI business usage is accelerating, with 78% of organizations reporting using AI in at least one business function in 2024, up from 55% the year before, competitive intelligence research remains in an earlier stage of adoption.

56% of our audience say artificial intelligence is not currently used, implying that many teams still rely on manual research processes or established analytical methods. 42% report experimentation and pilot use, showing growing interest as teams test how AI can support data gathering and insight generation without fully committing.

Automated data monitoring and analysis is only used by 1%, where AI begins to take on continuous tracking of competitors and market signals. Insight discovery and pattern detection are also used by 1%, representing the most advanced use, where AI is applied to uncover trends and connections that would be difficult to identify manually.

Sedulo Commentary: Sedulo sees AI as a valuable tool for accelerating competitive intelligence, but not as a replacement for experienced analysis or primary research. The strongest approach combines AI-enabled monitoring and synthesis with human expertise to validate findings, interpret implications, and translate signals into strategy.

How Frequently Does Your Organization Review Competitive Intelligence Research Insights?

40% of insights, strategy, or marketing leaders say that their organization continuously reviews competitive intelligence insights using monitoring tools

The frequency of insight reviews is crucial but not consistent across the board:

The frequency with which competitive intelligence research insights are reviewed among leaders in our audience varies, though continuous and structured approaches are common. 40% review insights continuously through monitoring tools, showing a shift toward real-time visibility of competitors and market activity. The U.S. Small Business Administration highlights that effective competitive analysis relies on consistent data collection and access to reliable research resources, which supports this kind of always-on approach

36% review regularly during strategy cycles, where intelligence feeds into planned decision-making points. 19% review occasionally during planning sessions, suggesting a more periodic approach tied to specific initiatives.

3% review rarely on an ad hoc basis, while another 3% only review when major market shifts occur, indicating a reactive use of intelligence rather than an ongoing process.

Sedulo Commentary: Sedulo believes competitive intelligence is most valuable when it functions as an ongoing system, not a periodic exercise. Continuous monitoring helps organizations identify early signals, respond to market shifts more quickly, and make strategic decisions with greater confidence.

How Does Your Organization Share Competitive Intelligence Research Insights Internally?

82% of leaders say their organization uses research reports to share competitive intelligence research insights internally

Sharing of insights internally is largely done through one channel:

The way that competitive intelligence research insights are shared internally among our audience’s leaders is guided by structured reporting. 82% use internal research reports, showing a clear preference for formal documentation that can be referenced across teams and used to support consistent decision-making.

Marketing and product workshops account for 11%, where insights are discussed collaboratively to align messaging, positioning, and development priorities. Informal knowledge sharing is used by 7%, likely a smaller number of teams relying on impromptu conversations, which can be quicker but less consistent in how insights are applied.

Sedulo Commentary: Sedulo sees structured reporting as essential, but the real value comes from making insights easy for teams to apply. The most effective CI deliverables do more than document findings, they translate intelligence into clear implications, decisions, and next steps.

Which Competitive Insight Area Receives The Most Attention In Your Organization?

80% of leaders say that market expansion and growth strategy is the competitive insight area that gets the most attention in their organization

One area gets the largest share of attention:

The competitive insight areas that receive the most attention are spread across multiple strategic fronts. Market expansion and growth strategy is the top priority for 14% of our audience, while 66% say it gets some focus, showing that most teams are applying competitive intelligence broadly rather than concentrating it in one area.

The U.S. Chamber of Commerce advises that effective competitor analysis involves assessing factors like product, pricing, positioning, and customer perception, which helps explain why attention is spread across different areas rather than being focused on just one.

Product innovation and feature strategy get some focus for 15%, where intelligence helps teams track competitor offerings and refine their own development priorities. Partner ecosystem and alliances get some focus for 5%, hinting that collaboration and external relationships receive more targeted attention within competitive analysis.

Sedulo Commentary: Sedulo views market expansion and growth strategy as a high-value application of competitive intelligence, especially when organizations are evaluating where to invest, enter, or defend. Strong CI helps leaders understand not only where opportunities exist, but also how competitors are likely to respond.

Which Type Of Competitor Activity Do You Monitor Most Closely?

100% of insights, strategy, or marketing leaders monitor strategic partnerships as a top priority

There’s one core competitor focus: Strategic partnerships are hugely beneficial to businesses, and collaborations between partners can greatly expand marketing reach and customer bases. It’s understandable, then, that 100% of the opinions of insights, strategy, or marketing leaders focus on this competitor activity and consider it a top priority.

Sedulo Commentary: Sedulo views strategic partnerships as an important early indicator of competitive intent, because they often reveal where a competitor is looking to expand, strengthen capabilities, or reposition in the market. Tracking these moves can help organizations anticipate shifts before they become fully visible in product, sales, or go-to-market activity.

Which Type Of Market Signal Provides The Earliest Indicator Of Competitive Change?

54% of leaders say that talent hiring trends are the earliest indicator of competitive change

Hiring trends are a top marketing signal of change:

The type of market signal that provides the earliest indicator of competitive change among leaders in our audience leans toward talent hiring trends, though views are mixed. Gartner’s Future of Work Trends for 2026 points out that organizations are rapidly rethinking hiring and reskilling strategies as new skills come into demand, which helps explain why changes in talent hiring can signal where a business is heading before those shifts become visible in products or market activity.

23% say talent hiring trends are the earliest indicator, while 31% describe them as a likely early sign, showing that many teams look to workforce changes for early direction.

At the same time, 42% say they are not the earliest, pointing to hiring signals being open to interpretation. Product development activity is seen as a likely early sign by 5%, indicating it is more commonly viewed as a later-stage signal once direction is already taking shape.

Sedulo Commentary: Sedulo views hiring activity as a valuable early signal, but it is strongest when analyzed alongside product development, leadership changes, investment priorities, and market activity. Taken together, these signals can help organizations identify where competitors may be placing future bets before those moves are publicly announced.

Which Type Of Competitor Insight Provides The Most Strategic Value For Your Team?

73% of leaders agree that product strategy insight provides the most value for their teams

One type of competitor insight provides the most team value:

The type of competitor insight that provides the most strategic value for leaders centers on product strategy insight. 16% of our audience says it is extremely valuable, 36% quite useful, and 21% somewhat useful, showing how closely teams track competitor product decisions to guide their own development and long-term direction. This kind of insight shapes what gets built, improved, or deprioritized.

Marketing messaging insight is seen as extremely valuable by 13%, quite useful for 2%, and somewhat useful for 4%, which points to a more targeted role in refining positioning and communication. Pricing and positioning insight is considered extremely valuable by 7%, where it supports decisions around competitiveness and perceived value in the market.

Sedulo Commentary: Sedulo sees product strategy insight as especially valuable because it helps organizations understand not only what competitors are building, but where they are prioritizing investment and how they intend to differentiate. When paired with pricing, positioning, and messaging analysis, product insight can give teams a clearer view of competitive direction and strategic risk.

Which Published Media Or Websites Provide The Most Valuable Competitive Insights For Your Team?

For 44% of leaders, The Wall Street Journal provides the most valuable competitive insights for teams

The media plays a major role in providing valuable competitor insights:

The published media and websites that provide the most valuable competitive insights for leaders in our audience deliver mixed levels of value. The Wall Street Journal stands out as one of the most widely used sources, with 2% calling it extremely valuable, 18% quite useful, 24% somewhat helpful, and 11% not valuable. As of 2025, it is the largest newspaper in the United States by print circulation, with 412,000 print subscribers, alongside 4.13 million digital subscribers.

Bloomberg is rated extremely valuable by 2%, quite useful by 11%, somewhat helpful by 8%, and not valuable by 4%, where it provides timely market and financial insight. Forbes sees 4% calling it extremely valuable, 7% quite useful, 3% somewhat helpful, and 2% not valuable, with content often centered on trends and leadership thinking.

TechCrunch is rated extremely valuable by less than 1%, quite useful by 2%, and somewhat helpful by less than 1%, reflecting its niche focus on startups and innovation. Harvard Business Review is seen as quite useful by less than 1%, where its value lies in deeper strategic frameworks rather than day-to-day competitive tracking.

Sedulo Commentary: Sedulo sees published media as a useful input, but not a complete competitive intelligence strategy on its own. The greatest value comes from combining public sources with primary research, market context, and structured analysis to understand not just what happened, but what it means for the business.

Which Resources Do You Rely On Most To Learn About Competitive Intelligence Research Best Practices?

The resources relied on most to learn about competitive intelligence research best practices among leaders in our audience lean heavily toward deeper, more hands-on learning. Business books and research reports are the top resource for 33% and a helpful source for 32%, showing how leaders build a strong foundation in competitive analysis frameworks, research methods, and structured approaches to gathering and interpreting market signals.

Professional training programs are the top resource for 32%, where practical application helps develop the skills needed to run competitive intelligence processes effectively. Industry publications and business media are the top resource for 4%, offering a lighter way to stay current but with less depth for building consistent CI practices.

Sedulo Commentary: Sedulo sees best practices as most valuable when they are paired with real-world application and tailored to an organization’s specific market, competitors, and strategic priorities. Competitive intelligence is not just learned through frameworks, but strengthened through disciplined research, structured analysis, and repeated use in decision-making.

What Challenge Most Often Limits The Effectiveness Of Competitive Intelligence Research?

Fragmented information sources are only somewhat of a challenge that limits the effectiveness of competitive intelligence research for 8% of leaders

Challenges limiting effectiveness are minimal:

The challenges that most often limit the effectiveness of competitive intelligence research among leaders in our audience appear less pronounced than wider industry trends would suggest. Wider industry analysis of competitive intelligence practices shows that 95% of CI professionals struggle with at least one core issue, with 52% citing difficulty in gathering competitive data, alongside challenges in measuring results, separating signal from noise, driving action, and organizing information.

Fragmented information sources are somewhat of a challenge for 8% of our audience, not a big challenge for 26%, and not a challenge at all for 29%, showing that many leaders are working with more structured and accessible data. Slow insight delivery is somewhat a challenge for 3%, not a big challenge for 6%, and not a challenge at all for 11%, pointing to generally efficient processes.

Difficulty translating insight into strategy is somewhat a challenge for 3%, not a big challenge for 9%, and not a challenge at all for 4%, where the link between insight and action still requires attention but is not widely seen as a barrier.

Sedulo Commentary: Sedulo often sees that the biggest challenge is not simply accessing information, but knowing which signals matter and how to translate them into strategic action. Effective competitive intelligence requires disciplined collection, careful interpretation, and clear recommendations that help teams move from awareness to decision-making.

Which Outcome Would Most Improve The Value Of Competitive Intelligence Research In Your Organization?

59% of insights, strategy, or marketing leaders say that deeper competitor analysis would make a huge difference to the value of competitive intelligence research in their organization

One outcome would provide the biggest improvement:

The outcome that would most improve the value of competitive intelligence research among leaders in our audience is deeper competitor analysis. 59% say it would make a huge difference, with a further 18% saying it would be a solid improvement, pointing to a need for sharper insight into how competitors operate, not just what they are doing.

Better integration with decision-making would make a huge difference for 3% and be a solid improvement for 9%, highlighting the importance of connecting insight more directly to action. Stronger strategic recommendations would be a solid improvement for 6%, where leaders are looking for clearer direction from the insights they gather.

Faster insight generation would make a huge difference for 2%, and clearer market opportunity signals would make a huge difference for 2%, showing that speed and clarity still play a role, even if they are not the primary focus.

Sedulo Commentary: Sedulo believes deeper competitor analysis is where competitive intelligence becomes most actionable, because it helps organizations understand the motivations, capabilities, and likely next moves behind competitor activity. The greatest value comes when that depth is paired with clear strategic implications that help leaders decide what to do next.

Which Format Makes Competitive Intelligence Insights Easiest For Leadership Teams To Act On?

100% of leaders agree that strategic insight presentations would be a fairly actionable format for making it easier for leadership teams to act on competitive intelligence insights

For all of our audience, strategic insight presentations are considered a fairly actionable format that makes competitive intelligence insights easier for leadership teams to act on. This is likely because they distill complex data into clear, structured narratives that highlight key takeaways and recommended actions, supporting faster, more confident decision-making.

Sedulo Commentary: Sedulo agrees that strategic insight presentations are highly effective when they move beyond summarizing data and clearly connect findings to implications, risks, opportunities, and recommended actions. Leadership teams are best equipped to act when competitive intelligence is presented as a decision-support tool, not just an information-sharing format.

Which Industry Does Your Organization Operate In?

87% of insights, strategy, or marketing leaders operate in the manufacturing and industrial sectors

Competitive intelligence is used extensively by major industries:

The industries in which insights, strategy, or marketing leaders in our audience operate are heavily concentrated in the manufacturing and industrial sectors. 87% fall into this category, showing how closely competitive intelligence (CI) research is tied to environments where supply chains, pricing pressures, and competitor activity directly influence performance. This also aligns with the sector’s scale. The manufacturing industry in the United States is valued at $6.9 trillion and is the fifth-largest employer.

Technology and software account for 13%, where competitive intelligence tends to focus on product positioning, rapid innovation cycles, and tracking competitor moves in fast-changing markets.

Sedulo Commentary: Sedulo sees strong competitive intelligence adoption in manufacturing and industrial markets as a reflection of how complex, competitive, and operationally sensitive these sectors can be. In markets shaped by supply chains, pricing pressure, product innovation, and competitor movement, timely intelligence can help organizations protect share and identify growth opportunities.

Which City Is Your Organization Primarily Based In?

47% of insights, strategy, or marketing leaders’ organizations are primarily based in San Francisco

Organization’s geographical locations are unevenly dispersed across the US:

The cities where organizations of leaders in our audience are primarily based is led by San Francisco. 47% are located there, showing a strong presence in a hub known for technology, innovation, and data-driven decision-making. New York follows at 39%, where proximity to major financial, media, and corporate markets supports a different but equally influential perspective on competitive intelligence.

Boston accounts for 12%, reflecting its strength in research, education, and emerging technology sectors. Los Angeles represents 2%, where competitive insight is likely more closely tied to media, entertainment, and creative industries.

Sedulo Commentary: Sedulo sees the concentration of competitive intelligence activity in major business hubs as a reflection of where fast-moving, data-driven organizations are often clustered. At the same time, competitive intelligence is valuable well beyond these markets, especially for any organization facing changing customer expectations, evolving competitors, or pressure to identify new growth opportunities.

Leaders Are Using Insight to Stay Ahead of Market Change

Looking across these findings, competitive intelligence research stands out as a practical driver of better decisions rather than a theoretical exercise. The analysis of these 949,079 opinions makes it clear that insights, strategy, and marketing leaders are refining how they gather, interpret, and apply insight to stay aligned with changing market conditions, while continuing to strengthen how intelligence supports everyday decision-making.

About The Data

Sourced using Artios from an independent sample of 949,079 opinions of insights, strategy, or Marketing leaders in the USA across X, Quora, Reddit, Bluesky, TikTok, and Threads. Responses are collected within a 95% confidence interval and 5% margin of error. Results are derived from what people describe online, from opinions expressed online, not actual questions answered by people in the sample.